UPDATE - By the skin of their teeth, House Republicans passed the American Health Care Act this afternoon. They had just one vote to spare; 20 members of the GOP conference voted no, along with every Democrat. The bill now advances to the United States Senate where inevitable changes will be made (see more analysis below). As I said on Fox News as the news broke, this is the legislative equivalent of a first down -- but not a touchdown. More work is needed, as I've outlined in this piece. The House also unanimously passed a measure explicitly not exempting themselves from the law, which fixes the issue raised here. It's a big day, but there's an arduous road ahead for this legislation.

In March, they didn't have the votes, and the bill was pulled. Today, they appear to have the votes, so they're moving forward on the floor. I have both practical policy concerns about the legislation, as well as good-government procedural objections to the nature of the process -- but let's start with what is actually in the refurbished American Health Care Act:

INDIVIDUAL MARKET: The AHCA repeals Obamacare's individual mandate tax, which requires every American to purchase a product, fining millions who won't or cannot afford to comply. It rolls back the employer mandate, which has had negative economic impacts, including curtailing some workers' hours. It rolls back, repeals, and delays many of Obamacare's taxes, such as the innovation-stifling medical device tax. It undoes the current law's subsidy system starting in 2020, replacing it with an "age-adjusted, advanceable, refundable" refundable tax credit for individuals and households, raging from $2,000 to $14,000 per year (with generosity levels phasing out for wealthier recipients). It doubles the allowed tax-free annual contribution to Health Savings Accounts, and it shifts the ratio of "age bands" to pre-Obamacare levels, allowing carriers to offer cheaper plans to younger consumers.

MEDICAID REFORM: The AHCA grandfathers in everyone who has been included in Obamacare's expansion of Medicaid, then "transition[s] Medicaid into a system in which each state receives a certain amount of money for each of its residents in the program and has more flexibility over how the program functions. That allocation would revert to per person spending levels from 2016 and then grow each year at the rate of medical inflation. However, states would still receive enhanced Obamacare-levels of spending for individuals who were grandfathered in by having enrolled in expanded Medicaid before 2020." Medicaid already suffered from major flaws such as poor health outcomes and seriously constricted access to care before Obamacare expanded it significantly. One-in-three doctors are not accepting new Medicaid patients. The status quo is hugely expensive, putting major strains on state budgets, and not working well. The whole program cries out for reform, which the AHCA delivers.

PRE-EXISTING CONDITIONS: The legislation maintains several of the more popular mandates and protections under Obamacare (although it's worth noting that some of those requirements become much less popular once people are told how much they cost). People with pre-existing conditions must be covered, adult children can stay on their parents' plans through age 26, coverage plans must comply with Obamacare's categories of "essential health benefits," and consumers with pre-existing conditions cannot be charged more than others. On the latter two mandate categories, states have the option to seek waivers from some of the EHB's and "community rating" restrictions. In order to be granted a waiver, states must attest and demonstrate that they are doing so in pursuit of lowering premiums and/or covering more people. Recall that before Obamacare, every single state had a set of mandates and regulations in place. So even if some states apply for and receive voluntary waivers, there will be protections and requirements for consumers who live there. Fear-mongering about a return to the "wild west" are exaggerated.

No matter where they live, anyone who has continuous coverage (including people with pre-existing conditions who signed up for plans under Obamacare) cannot be impacted by a "community rating" waiver, immediately or in the future. And those consumers without coverage who decide to obtain it must be able to purchase to it. Average consumers who do this will be charged a one-time 30 percent surcharge on their plan for one year. Consumers with pre-existing conditions must have access to a high risk pool, which will be especially important in so-called waiver states. The AHCA directs upwards of $130 billion to these and similar funds. I strongly recommend this piece by Avik Roy, who argues that the fixation on pre-existing conditions (a worthwhile and compassionate concern) has taken on an outsized role in these debates. Part of his evidence is the fact that enrollment in Obamacare's "bridge" program to help bring Americans with pre-existing ailments into the insurance fold between the law's passage in 2010 and implementation barely broke into six figures.

POLICY CONCERNS: This legislation is far from perfect, and the Senate's open-ended amendment process must and will be used to alter the bill. My biggest worries about the policy impact are as follows. (1) It's widely recognized that a critical mass of older Americans approaching retirement age will be priced out of affordable plans, based on the level of assistance provided in the AHCA tax credits. Axios reports that GOP Senators, led by John Thune, plan to address this shortcoming. It is an urgent priority. (2) I've been told by senior Republican sources that health insurance actuaries have blessed the '30 percent surcharge' mechanism for incentivizing continuous coverage (especially among younger, healthier people) as effective, but I remain skeptical. If the only slap on the wrist for waiting to get sick or injured before showing up to buy "insurance" is a one-time, quickly-expiring uptick in cost, why wouldn't these consumers just save the money and wait?

This is precisely the dynamic that is dooming Obamacare's risk pools. More affordable, less mandate-laden coverage offerings to younger folks may attract more 'young invincibles' to the market, but the Senate should explore whether or not pro-rating the surcharge to reflect the amount of time a new consumer was uninsured might work better. This idea from two conservative policy experts, featuring automatically enrolling people (with an opt-out) into basic plans with costs that align with their tax credits, should also get a look. Cost could be a problematic factor, however. (3) Despite several layers of pre-existing condition protections, some studies suggest that even the AHCA's nine-figure allocation for high risk pools may not be sufficient to help those who fall through the cracks. The issue is that we don't know what the patchwork of waivers might look like. Experts should be consulted on this matter, taking into account the number of currently-uninsured people with pre-existing conditions living in states most likely to pursue "community rating" waivers.

PROCESS CONCERNS: The House's legislative process has been a mess. Having had years to develop a unified Obamacare alternative (I'd note that many bills were filed, in spite of the Democratic talking point that Republicans had "no ideas"), the GOP struggled to rally around a bill that achieved key goals and attracted the support of various factions of the party. The March debacle was a nadir. Now, the House is going to vote on a bill without the finalized text being available to the public (or even members!) for any reasonable amount of time, and without a fiscal score from the Congressional Budget Office. This is bad practice and bad precedent. Yes, CBO's projections on Obamacare have been pretty terrible on several key measures, and its preliminary judgments on the AHCA were overly alarmist, but those are not good enough excuses. In fact, the lack of a CBO score will likely delay any action in the Senate. If the upper chamber eventually passes an updated (and I'd guess significantly revamped) bill later this year, there must be a CBO score prior to final passage. The healthcare sector represents one-sixth of the US economy. I'll leave you with a flashback to Paul Ryan rightly complaining about Democrats' legislative methods in 2009, as well as the latest drop in the drip, drip, drip of Obamacare's ongoing failure:

Paul Ryan in 2009: "I don't think we should pass bills that we haven't read that we don't know what they cost." #Awkward pic.twitter.com/7AA9i1McqN

— Josh Jordan (@NumbersMuncher) May 4, 2017

Aetna pulls out of Virginia's individual market, citing big Obamacare losses https://t.co/By1Oz8WBKy

— Jake Tapper (@jaketapper) May 3, 2017

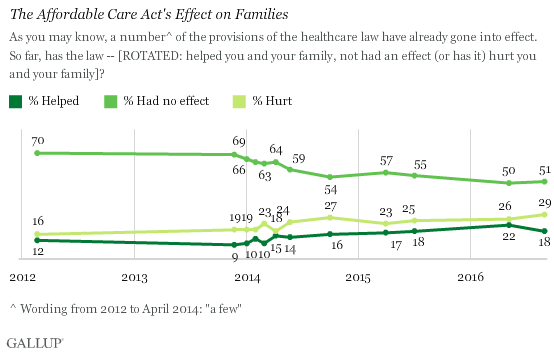

The American Health Care Act is flawed and needs fixing. It will not become law as-is, period. Republicans campaigned on uprooting and overhauling Obamacare for seven years, winning three national elections in the process. They must deliver on their promise because the alternative would mean the abandonment of millions of people being harmed by the imploding status quo. Data has consistently shown that Obamacare has hurt more people than it's helped. Today's vote, assuming passage, is an important first step in the process of cleaning up the unsustainable mess created exclusively by Democrats in 2009 and 2010. Yes, it is fraught with political risk, but so is failing to act. Moving forward, Republicans must be open to empirical data and expertise in plugging policy holes in this proposal. They must be cognizant of the reality that healthcare policy impacts real people in real ways. They should also not retreat in the face of nasty, demagogic hyperventilation from the Left, which is screaming about GOP policies 'killing' people. As a reminder, though the Democrats' law has undoubtedly helped some Americans, the evidence shows that it not been a life-saver in the aggregate -- with death rates increasing (at a higher rate in Medicaid-expanding states, by the way) and American life expectancy dropping for the first time in decades since its implementation. Finally, this is misleading:

JUST IN: ObamaCare repeal bill contains exemption for members of Congress and their staffs https://t.co/zgKH5p94PM pic.twitter.com/aOW0RYXaXE

— The Hill (@thehill) May 4, 2017

Here's my reporting and explanation on why.

{kind=link}

Join the Conversation

VIP members get the ability to comment on articles.