After years of (quite successfully) campaigning against Obamacare, Republicans have finally unveiled "unified" legislation that would "repeal and replace" the failing law. Why the scare quotes? Because based on early indications, the GOP is hardly unified behind the plan -- despite the enthusiastic endorsement of leadership in both houses of Congress, the HHS Secretary, and the President of the United States. Indeed, some of the bill's conservative critics wouldn't even concede that the proposal amounts to a genuine repeal and replacement of the existing law. The Left, meanwhile, is savaging the plan with their usual parade of horribles (heartless, sexist, etc), while also smirking that it's somewhat similar to Obamacare. This pivot from "these Republican clowns have no plan!" to "these Republican demons have a vicious, murderous plan!" was as predictable as the run rising in the east. Amid all the sound and fury, what should conservatives make of all of this? Let's examine what the proposed bill does, and does not, seek to do:

What conservatives will like: Compared to Obamacare, GOPCare reduces the role of the federal government in the healthcare system, gives more authority and flexibility to states, spends less, taxes less, regulates less, and coerces less. The individual and employer mandates are gone. Infamous tax hikes like the medical device tax are gone (and in other cases, delayed or reduced). Obamacare's subsidy system is dismantled by 2020 and supplanted with refundable tax credits for lower-to-upper-middle-income individuals and families, ranging from $2,000 to $14,000 annually. Granted, this is not a universally-beloved solution on the Right, though some of its critics very recently co-sponsored replacement legislation under which refundable tax credits were a centerpiece. Caps on tax-free contributions to Health Savings Accounts are also raised considerably, almost doubling under this bill. The conservative Republican Study Committee is out with a pretty balanced memo on the positives and negatives of the draft legislation, noting several shifts towards more coverage and more spending over the weekend.

Provisions designed for political palatability and to blunt attacks: Three of the (precious few) elements of Obamacare that are actually broadly popular with the American people are preserved in GOPCare. People with pre-existing conditions are protected. With the individual mandate tax gone, the law would safeguard anyone who buys and maintains continuous coverage; for those whose coverage has lapsed for at least two months, insurers would be permitted to apply a 30 percent surcharge for a year if that person seeks to sign up. This incentive structure maintains the dynamic of an insurance market, as opposed to straight-up welfare. But will it work to improve upon Obamacare's toxic "adverse selection" risk pool problem? Some experts are skeptical, and their concerns should be addressed. Also, lifetime expenditure caps from carriers remain disallowed, and adult children are permitted to remain on their parents' plan through age 26. Beyond that, the tax credits mentioned earlier will increase with age, but phase out as recipients' incomes cross the $75,000 threshold for individuals and $150,000 for families. The wealthiest Americans are ineligible for tax credits, as are any consumers who are offered employer-based coverage or other forms of government healthcare. The plan also proposes spending $100 billion on a "patient and state stability fund," earmarked for states to experiment with best practices to cover low-income Americans who have been perennially difficult to insure. This fund will also help address the pre-existing conditions dilemma by encouraging and funding innovation in the states.

Recommended

The thorny Medicaid question: One of Obamacare's most controversial items was the expansion of Medicaid, a massive and costly program for indigent (and now less-indigent) Americans that was already struggling mightily with poor health outcomes and major access problems before Obamacare funneled millions of additional people into it. Fiscal conservatives opposed the expansion altogether, but a number of Republican governors chose to take the federal money, even with strings attached. What happens to the Medicaid expansion under GOPCare? Obamacare's status quo would remain in place until 2020, at which point the new law would "transition Medicaid into a system in which each state receives a certain amount of money for each of its residents in the program and has more flexibility over how the program functions. That allocation would revert to per person spending levels from 2016 and then grow each year at the rate of medical inflation. However, states would still receive enhanced Obamacare-levels of spending for individuals who were grandfathered in by having enrolled in expanded Medicaid before 2020," as summarized by Philip Klein. Many conservatives want the Medicaid expansion done away with entirely, but a group of four GOP Senators just wrote a letter warning that they'd vote against any plan that tinkered too much with the current policy, urging 'security' for citizens already in the system. Does the just-announced bill, with its grandfathering and years-long phase-out, represent sufficient flexibility for these recalcitrant Senators? And are these cross currents within the party reconcilable? I guess we'll see.

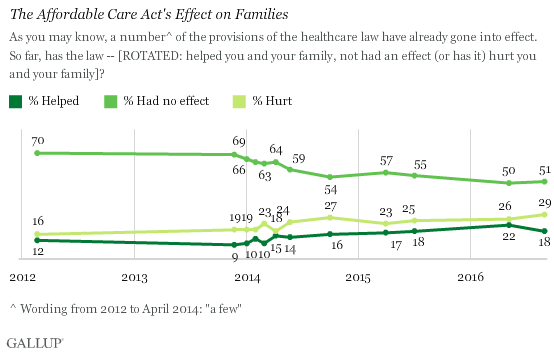

Challenges: How much will this bill cost, and how will it be paid for? Plus, despite being much less expensive than Obamacare, if the math doesn't add up, will the Congressional Budget Office score it as a deficit-increasing endeavor? We don't know those answers yet. And even though the bill goes much farther than many conservatives would like in terms of expenditures, liberals are already expressing outrage that its CBO score will likely show that the number of Americans with coverage would be reduced if GOPCare is implemented. Of course "let's cover as many people as possible" was not the primary mantra used to sell Obamacare; affordability was, hence the "Affordable" Care Act misnomer, and the accompanying wave of broken promises about substantially lower premiums and out-of-pocket costs. But reduced coverage levels will be a central talking point used by Obamacare defenders to scare Americans into believing that the Republican plan would rip coverage away from millions (although that's precisely what Obamacare did to millions of people who'd been lied to about being allowed to keep their existing plans and doctors if they so chose). Republicans should focus on the cost-reducing and choice-increasing aspects of their plan. It's about improving access to care.

Some people may notice that certain important solutions that have been discussed before -- like allowing the purchase of insurance across state lines and medical malpractice reform -- aren't in this legislation. Why? Because the "reconciliation" maneuver to bypass the filibuster can only be applied on budgetary matters. Other legislative changes to the law would be subject to clearing the cloture bar, which requires 60 Senate votes. That's why the reconciliation package is merely the first of three steps in this process: (1) Cramming as much 'repeal and replace' into the reconciliation bill as is legal under the rules, (2) Sec. Price making cost-reducing adjustments through unilateral HHS regulations, and (3) traditional legislation. As for coverage rates, it's worth noting that Obamacare has failed badly to achieve projected enrollment numbers. When it passed, CBO estimated that 21 million Americans would have signed up for coverage through the law's exchanges by 2016. Last year, they slashed their own estimate by 8 million -- and still overshot the mark. Nevertheless, Philip Klein and some liberals already see a potential political trap Republicans may be setting for themselves by scheduling some of the biggest changes to kick in on January 1, 2020. On one hand, this adjustment period of three years is meant to assure voters that the transition will be stable, not sudden. That's understandable. On the other hand, is it risky to schedule tapered "cliffs" for an election year?

Obamacare's two major spending provisions will carry on for nearly the next three years, and millions more people could theoretically be signing up for coverage through the program during this time. Republicans, who are struggling to handle the messaging about Obamacare beneficiaries losing coverage, would be setting themselves up so that the brunt of any disruption would be happening in January of an election year in which they'd be defending the Senate seats they won in their wave election year of 2014. The party would also have to be defending the presidency and fighting over control of the state governments that will redraw the boundaries for Congressional districts, which will have a major implication on House control in the coming decade...This could set up a situation similar to the "fiscal cliff" surrounding the expiration of the Bush-era tax cuts at the start of 2013, with legislatures scrambling in the wee hours to come up with a compromise. It's easy to see how lawmakers could just get together and decide to punt on the issue until after the presidential election.

That scenario, in turn, could lead to a routine of kicking the can down the road, rather than allowing the buck to stop long enough for political blame to attach. Think that's unfathomable? Google the Medicare "doc fix."

Bottom Lines: As I've been saying for some time, the only shot Republicans have at uprooting Obamacare is if they're unified on substance and effective in their messaging. Neither of those prerequisites are being met thus far. Moderates are publicly wringing their hands about more robustly enshrining Obamacare's Medicaid expansion, while conservatives are blasting the proposal as too costly and too similar to Obamacare. (Klein makes the point that the baseline of public expectations set by Obamacare, and the GOP's efforts to reckon with that political reality, demonstrate that even if the law is rolled back in major ways, Obama will have advanced the ball for liberalism and statism in the long run). So on one end of the spectrum, you have centrists who want to tinker at the edges and pretend that's "repeal." They will not vote for a plan that doesn't cover of a lot of people. On the other end of the spectrum, there are conservatives demanding that Congress simply repeat its repeal vote of 2015, then figure out a replacement plan some other time. Their theory is that once the law is truly gutted, everyone's incentives shift to getting serious about finding a solution to stave off inevitable market chaos.

That may make some sense in theory, but it very well may not in practice. Democrats have already announced that their intention would be to block any solution and blame the widespread upheaval on Republicans. And why should anyone expect that Republicans would magically find a way to unite in the future when they've been unable to do so for the last seven years? And by the way, now that there's a president waiting to sign a repeal bill into law, a number of moderate Republican members simply won't be willing to support a "repeal, don't replace" game plan. These votes aren't symbolic anymore. We're firing live ammo now, they'll say, and we promised people a stable replacement. What they may decline to add, to Klein's point, is that the American electorate's appetite for small government libertarianism (especially on healthcare) is rather limited. That's a painful reality for those of us who believe in markets, but it's a reality nonetheless. Relatedly, it must also be said that some of the new voices now demanding that Congress go the 2015 repeal route without a replacement were (very recently) adamant that repeal and replace must be done in tandem, virtually simultaneously.

In short, the Democratic Left will circle the wagons around President Obama's biggest legacy item, while the Right risks tearing itself apart. If that dynamic holds, Obamacare will prevail -- which would be terrible news for the millions of Americans being actively harmed by that increasingly-deteriorating law. It would also represent a horrendous betrayal of the millions of voters who repeatedly elected Republicans on the promise that they'd repeal and replace Obamacare -- if only they had both houses of Congress and the White House. That moment has at last arrived, yet the GOP's ideological divides could cause that long-awaited vow to implode on the launching pad. It's premature to make any declarations about where this path will end up. There will be committee mark-ups and amendments in both houses of Congress as this process unfolds, so hopefully a viable consensus can be forged. The first draft isn't necessarily the end-all-be-all, but Speaker Ryan's office emphasizes that the crafting of this bill is the result of months of collaborative meetings and discussions with the entire caucus -- with heavy input from the White House. The stark truth is that a splintered GOP will guarantee Obamacare's survival. The law would wither painfully on the vine for years, hurting more and more people as it collapses. Republicans have said this is unacceptable and have pledged to end the law as it exist and replace it something better. Now that they have the means to do just that, will they keep their promise, or will they choke? I'll leave you with word out of the White House, as well as the first salvo in a blitz to pull reluctant members aboard:

White House official tells me President Trump is "all in" on Ryan health care bill, "100 percent."

— Eamon Javers (@EamonJavers) March 7, 2017

Included in @AAN's first pro-AHCA blitz are districts held by Republicans who oppose the bill. => https://t.co/4JukKT8SBm

— David M. Drucker (@DavidMDrucker) March 7, 2017

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Join the conversation as a VIP Member