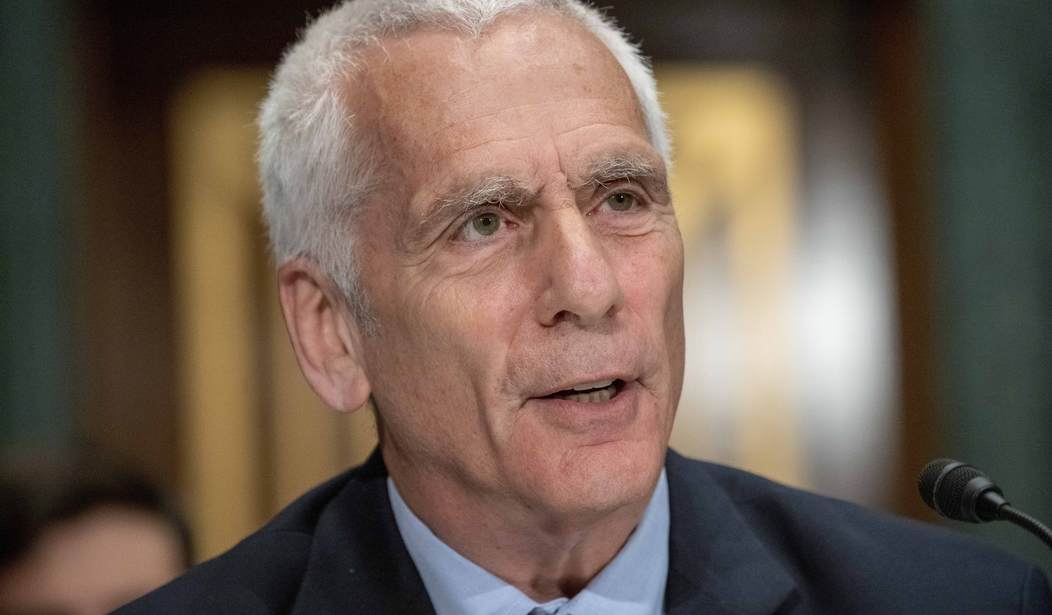

The Biden administration is looking to confirm yet another radical nominee, only this one is a rather familiar face looking to get promoted for failed economic policies. On Thursday, the Senate Committee on Banking, Housing, and Urban Affairs will vote on Jared Bernstein, who is a member of the Council of Economic Advisers (CEA), and has been nominated to be the chair of the CEA. Readers will know him for seeking to redefine what constitutes a recession, as well as defending the administration on gas prices and the economy overall. POLITICO profiled him in December of 2021 as "The man behind Bidenomics." The Atlantic even profiled him just before the 2020 election, as "Joe Biden’s Man on the Left."

A major problem plaguing the Biden administration has been inflation. Remember we were told “inflation is transitory?” Bernstein is actually one of the main figures behind such an idea, and his remarks are highlighted in the POLITICO piece above. He acknowledged the use of the term during a press briefing last July, when he spoke to "the ambiguity about the length of that word."

Biden Economic Adviser Jared Bernstein on the administration having previously defined inflation as transitory:

— Townhall.com (@townhallcom) July 18, 2022

"The lack of specificity about the cadence that was implied by that word, the temporal cadence implied by that word, led to a level of ambiguity..." pic.twitter.com/f0iWcvCRxl

This all appears to be a pattern. In a tweet from March 31, the American Accountability Foundation also highlighted all the instances in which Bernstein has made such a claim, as they proclaimed "He ought to resign in disgrace instead of leading the CEA!"

🚨 MUST SEE: Biden's nominee to lead the Council of Economic Advisers, Jared Bernstein, was COLOSSALLY wrong about inflation.

— American Accountability Foundation (@ExposingBiden) March 31, 2023

He ought to resign in disgrace instead of leading the CEA!

He must withdraw his nomination!! @econjared46@econjared pic.twitter.com/mI3nqQxAKe

He also got it wrong on inflation concerns as it applies to the American Rescue Plan Act (ARPA) and Build Back Better, having been quoted by numerous outlets dismissing the notion that such pieces of legislation would worsen inflation. As we now know, though, the ARPA indeed led to higher inflation, as even some fellow Democratic economists, such as Larry Summers, had warned it would. While Build Back Better never came to be, the misnamed "Inflation Reduction Act" did.

We may have Bernstein to thank for that, given his support for a so-called "can do economics" strategy that is just chock full of government intervention policies. "Minimum wage increases, budget deficits, low unemployment, industrial policy and so on not only can have their intended effects; they are necessary to offset structural economic inequalities," Bernstein claimed in an op-ed for The Washington Post, "Economics used to be all about what we can’t do. That’s finally changing," from December 2, 2019.

The op-ed was just full of other problematic ideas, including how he downplayed concerns with inflation:

In contrast with the old school [free market economics], can-do economics firmly rejects the assumption that the private economy will automatically settle into optimal conditions that policy actions can only distort. The central economic assumption must flip from equilibrium to disequilibrium. For example, we cannot assume “the market” will deliver full employment. In fact, while can’t-do economics was obsessed with preventing inflation, can-do economics is obsessed with getting to and staying at full employment. It begins from the recognition that power imbalances and excesses of unregulated capital will leave out large groups of people (often based on racial differences), inflate credit bubbles and pollute the environment. In can-do economics, market failures are not the exception. They’re the rule.

When we fast forward to how Bernstein handled the issue of inflation during his confirmation hearing on April 18, his responses were shocking. He again tried to hide behind how the term was "ambiguous," as he did with Sen. Katie Britt (R-AL), though he did ultimately respond in the affirmative to the senator's question that inflation "lasted longer than you anticipated when you first used that term."

Upon being questioned by Sen. John Kennedy (R-LA), Bernstein again hid behind the idea that it was "ambiguous" to say "inflation is transitory." Upon being asked by the senator "are you telling me that when you said inflation was transitory, you were correct," he couldn't answer. "No, I'm not saying I was correct or incorrect," Bernstein offered.

His positions on taxes are alarming as well. Such progressive views, a descriptor he seems to wear with a badge of honor, are on display in one of his op-eds from The Washington Post, in this case, one from September 25, 2017, "Democrats, don’t make the same mistake Republicans keep making."

In it, he argues that "The goal of progressive tax reform is simple: reduce pretax inequality and raise ample revenue to meet the known challenges faced by the public sector, including our aging demographics, climate change, geopolitics, rising health costs and helping those left behind even at low unemployment. This implies raising more revenue, and not solely from the top 1 percent, though that’s the right place to start. It means introducing a carbon tax and a small tax on financial transactions..."

A deep look at Bernstein's economic policies shows that, while these positions he holds on inflation and taxes are concerning, this just skims the surface. The op-eds he's written or news articles he's been mentioned in calling for an overhaul of various other areas of the economy are numerous.

There's a noticeable pattern here, too, as, in case you haven't already figured it out, Bernstein looks to focus on the issue of "equity."

One radical idea was expressed in one of his op-eds for The Washington Post, "The built-in biases in economics that feed systemic racism," from July 7, 2020. It's not just the headline that's problematic, though it certainly is. "Truly repairing the system obviously goes far beyond rejecting and replacing the economic model. Doing so is necessary, but not sufficient. Still, if we hope to expand the analysis of the economy to include the historical plight of those our system has long left out, we must thoroughly reject a model that not only ignores them, but builds the injustices they’ve long suffered into its core," Bernstein wrote at one point.

In a perspective from June 15, 2020, Bernstein co-authored "The Federal Reserve could help make the job market fairer for black workers" with Janelle Jones for The Washington Post. As one would expect, the radical ideas mentioned in the piece abound. The crux of the piece, and of a paper the two also co-wrote, is to focus on addressing the unemployment rate for specific races:

Yet in a recent paper, we argued the Fed should take on another task: delivering more racial equity into the labor market by, as we put it, “targeting not the overall unemployment rate, but the Black rate.” What does this imply, how would it help, and is it a reasonable ask of the independent central bank?

...

Because the Fed’s monetary policy partially sets the unemployment rate, it must be drafted to correct this persistent economic injustice. But operationally, how can it do so while maintaining its political independence and achieving its dual mandate?

In fact, what we’re proposing is handily within its scope and simply broadens the Fed’s mandate to make it more racially inclusive.

...

We propose that Congress add language requiring the chair to report on the extent of racial employment and wage gaps, and what the central bank is doing to reduce them (to be clear, we’re referring to all racial gaps, not just those of blacks). The chair should be required to report on these activities in his or her spoken and written testimony.

Note that our suggestion requires the Fed to report on actions it is taking to reduce these gaps. The language is far from neutral. It is not just asking the chair to tell us about the gaps; it requires him or her to make closing them a part of their mandate. Interest rate policy is paramount in this regard, but so is internal research on the causes of the gaps, and other, less well-known Fed activities such as the promotion of financial literacy, tracking economic stability of vulnerable families and access to affordable capital, including housing, for disinvested communities.

In case there is any question as to if this is front and center for the Biden administration, Bernstein cleared that up in another op-ed for The Washington Post from December 3, 2020, "I’m joining Biden’s economics team. Here’s some of what I’ll be thinking about." In referencing the above column, he pointed out "I’ve also pushed the Fed to go further, writing with Janelle Jones about ways the central bank can work to close persistent racial job, wage and wealth gaps. Importantly, this idea been adapted in Biden’s far-reaching racial inclusivity agenda."

These are just the more recent examples, as Bernstein had also argued a similar point in an op-ed he co-authored with Ben Spielberg for The American Prospect, "Does the Fed Think Black Lives Matter?," published on July 11, 2017.

"Yes, the central bank must manage its dual mandate: full employment at stable prices. But especially given the low correlation between inflation and unemployment in recent decades, the Fed would do well to consider the racial impacts of its decision-making," they wrote.

In 2017, Bernstein was quoted as coming out in favor of a $15 minimum wage and "a guaranteed jobs policy." He also wrote about as much in one of his op-eds for The Washington Post at the time, including where he mentioned the "Democrats need to come out swinging with a guaranteed jobs program."

Bernstein and his co-author Spielberg were especially blunt in another op-ed for The American Prospect, "The Progressive Agenda Now: Jobs and Medicare for All," also from 2017. "To win over and mobilize the public… we need a simple, plausible plan that excites people. Two key components of that plan are Medicare for All and a guaranteed jobs program," they wrote, getting to the heart of their headline.

Given his radical views, it sure looks like Bernstein fits right in with the Biden administration, including and especially on all things to do with that buzzword of "equity." Unfortunately, the American people are likely to suffer all the more for it if Bernstein receives a promotion.

Thursday's likely partisan vote will certainly be an interesting one to see.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Join the conversation as a VIP Member