A follow-up to my Obamacare post from yesterday: The law's adverse selection problem doesn't just inflame the risk of a market death spiral. It also all but guarantees that next year's expected premium hikes will be worse than anticipated for millions. The New York Times' lede is telling:

People signing up for health insurance through the Affordable Care Act’s federal and state marketplaces tend to be older and potentially less healthy, officials said Monday, a demographic mix that could threaten the law’s economic underpinnings and cause premiums to rise in the future if the pattern persists. Questions about the law’s financial viability are likely to become the next line of attack from its critics, as lawmakers gear up for the midterm elections this fall.

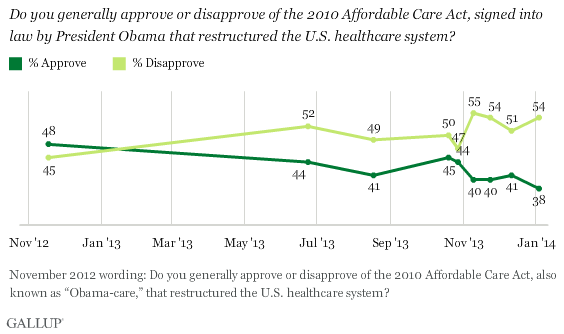

The law's "critics" include a substantial majority of the American people, most of whom would prefer not to pay significantly more for coverage under the auspices of a law called the "Affordable" Care Act. The Associated Press pores over the administration's demographic figures (which may not deserve to be taken at face value, given the White House's recent statistical distortions):

It's an older, costlier crowd that's signing up so far for health insurance under President Barack Obama's law, according to government figures released Monday. Enrollments are lower for the healthy, younger Americans who will be needed to keep premiums from rising. Young adults from 18 to 34 are only 24 percent of total enrollment, the administration said in its first signup figures broken down for age, gender and other details...While 24 percent is not a bad start, say independent experts, it should be closer to 40 percent to help keep premiums down. Adults ages 55-64 were the most heavily represented in the signups, accounting for 33 percent of the total...Some questions remained unanswered. For example, the administration is unable to say how of many of those enrolling for coverage had been previously uninsured.

And the demographic mix is even more toxic in some states than others. Remember, between four and six million Americans have been dropped from their existing coverage (so far), whereas just over two million had supposedly selected Obamacare plans as of the first of the year. Both the administration's private enrollment and Medicaid expansion figures appear to be massively embellished; it's a near certainty that Obamacare has resulted in a net increase in America's uninsured population -- a staggering failure, to say nothing of higher national costs and rising premiums. Democrats sold their trillion-dollar boondoggle on the promises of sharply decreasing the uninsured population while bending the country's health spending cost curve down, reducing healthcare-related deficits, and lowering annual costs for average families by several thousand dollars. And those weren't the only fantastical pledges they made. Reason's Peter Suderman strolls down memory lane and dredges up a few classics. Here's one of my favorites, which has been debunked by the CBO, and looks even more ridiculous in light of last month's dismal jobs report:

5. “It will create 4 million jobs-400,000 jobs almost immediately.”It wasn’t enough to pitch Obamacare as a premium-reducing law that would not have any negative consequences. Democrats also argued that it would create jobs. “This bill is not only about the health security of Americans,” Rep. Nancy Pelosi (D-Calif.), then speaker of the House, said in February 2010. “It’s also about jobs. In its life, it will create 4 million jobs-400,000 jobs almost immediately.” Reality: The gush of jobs never materialized. The unemployment rate slowly receded in the months after Obamacare passed, but largely because more people had quit searching for work. By 2021, according to projections by the Congressional Budget Office, the law is expected to shrink the nation’s work force by about 0.5 percent, since fewer people will hold onto their jobs to maintain their health insurance.

Healthcare wonk Avik Roy summarizes the major takeaways from Monday's data release: "[Estimated 2.4 percent losses] may seem like a small number, but given that the average insurer has profit margins of 4 to 6 percent, a 2.4 percent loss on premiums—before we even count overhead costs—is a serious problem. It’s why Humana reported to the Securities and Exchange Commission that it expected meaningful losses in its exchange-based plans...Taxpayers will be on the hook for any increased costs. Most importantly, many Americans will choose to go without insurance because it’s even less affordable than it was before." Congressional Republicans are angling to mitigate the "taxpayers on the hook for losses" issue, with Sen. Marco Rubio reprising his call for Washington to reject any and all Obamacare bailouts. I'll leave you with Charles Cooke marveling at lefties' ability to turn around and embrace their own Obamacare lies, which until recently drew howls of smear-mongering racism.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Join the conversation as a VIP Member