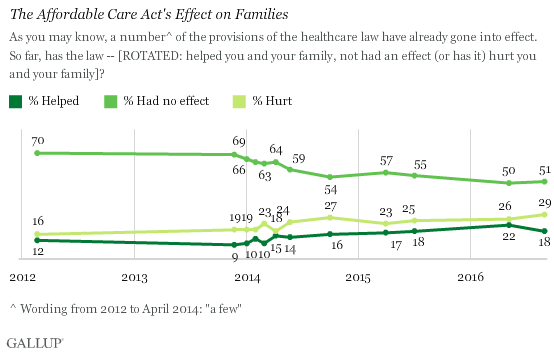

They essentially told Americans that there would be no losers under their scheme; people who liked their existing doctors and plans could keep them, and everyone else would finally have access to affordable care, with plenty of choice and competition -- all while premiums fell for everybody, with America's overall healthcare spending cost curve being bent downward in the process. None of that happened. Millions were ripped away from their plans, and millions more remained uninsured due to high (and rising) costs for most consumers. Many have also endured slashed options and access, and the cost curve is still pointing upward. It's that canyon between claims and results that crushed Democrats' credibility with many voters, and they've been punished at the polls ever since. Sec. Price is well aware of all of these dynamics, which makes the decision to go with this assertion such a head-scratcher:

An unforced error. Allahpundit is undoubtedly correct that Democrats and the press will tee up this soundbyte on a regular basis, especially to juxtapose it with an anecdote of an individual or family whose financial bottom line would (or does)

Insurance giant Anthem lent its support to parts of the Republican health care bill, saying changes must be made as soon as possible for the Obamacare [individual] market to survive. The company warned two Republican House committee leaders Thursday that without "significant regulatory and statutory changes," it will begin to "surgically extract" itself next year from the 14 states where it participates on the individual market. The company highlighted that it's the sole carrier in about one-third of the counties in those states, most of them rural. Anthem noted that it must start making decisions about its continued involvement in the exchanges as soon as mid-April. "The time to act is now," wrote Joseph Swedish, Anthem's CEO. "The American Health Care Act addresses the challenges immediately facing the individual market and will ensure more affordable health plan choices for consumers in the short-term, including through the expanded use of health savings accounts."

This is an encouraging sign for the AHCA, and a welcome bit of news for Republican leaders who've seen their legislation battered by criticism from the left and right. This week's Congressional Budget Office score of the bill is expected to show significant cost savings and potentially lower costs to many -- but not all -- consumers. Don't forget that additional cost reduction steps to be taken by Sec. Price's executive guidance ("phase two") and included in supplementary legislation ("phase three") will not included in CBO's calculations. And no, it's not unfair to remind the public that CBO, whose work is valuable and done in good faith, did badly miscalculate several of its most consequential Obamacare projections. Nevertheless, some of the CBO-related headlines are going to look scary, and Republicans must reassure people by explaining the realistic objectives of their solutions. This can include an acknowledgement that yes, some people will not keep their current plans, and that the percentage of insured citizens will inevitably decrease after the federal government stops forcing people to buy insurance (which far too many people have discovered is basically useless, due to access problems and exorbitant out-of-pocket expenses).

They can also note that people who have signed up for Medicaid within the Obamacare expansion are grandfathered in, despite some needed changes to the structure of that program in the future. There are legitimate answers to be given, but they ought to at least be plausible. I'll leave you with two big policy challenges within the legislation: (1) Is the incentive structure for "young invincibles" sufficiently robust as to bring that demographic into the market in droves, as needed? The "surcharge" mechanism that we discussed at some length last week has some wonks wondering if it might actually have the (clearly unintended) opposite effect, by actually undermining risk pools even further. This must be addressed. (2) A consensus appears to be building among conservative health care experts that GOPCare falls problematically short in providing financial help to a sizable band of low-income Americans. Analysts James Capretta calls the ACHA "the right framework," but offers a series of suggested improvements, one of which addresses this issue:

The AHCA provides a new tax credit structure for persons who do not have access to employer coverage, ranging from $2,000 to $4,000 per person depending on age. This is roughly comparable to the tax benefit conferred on employer coverage and could be considered equitable for persons in the middle class. However, those amounts are probably not enough to ensure that those at the lowest end of the income scale can afford insurance. A person under 30 years old with income high enough to be ineligible for Medicaid but below approximately 200 percent of the federal poverty line (around $24,000 in 2017 for a single person) would receive a $2,000 tax credit. That could cover a high-deductible insurance plan, protecting them from major medical expenses. But paying the deductible and routine expenses of seeing physicians and getting prescriptions filled would be a struggle. The AHCA should be revised to provide additional support to lower-income families. That support could come in the form of somewhat more generous tax credits in this income range, or a block grant to the states which would be used to provide additional support to these households.

One of the options he floats is further supplementing the bill's "Patient and State Stability Fund," which is designed to help ameliorate this problem. Another route would be increasing the refundable tax credits to lower-income people on a sliding scale. But those fixes would drive up the cost of the bill, and could risk alienating conservative lawmakers who are already lukewarm at best. Policy problem, meet political problem. Regardless, making over-broad, Polyannish statements about the impact of healthcare legislation is a big no-no, even when the contradictions can be laid bare:

Price doesn't deny 60-year-old in WV making $30K would get $8K less to keep their plan - but says "nobody worse off financially" bc choice. https://t.co/hQ5C8UiLSK

— Steven Dennis (@StevenTDennis) March 12, 2017

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Join the conversation as a VIP Member