Financially illiteracy is widespread—especially in the halls of Congress. The recently proposed Veterans and Consumers Fair Credit Act is the latest example. In Washington’s time-honored tradition, the bill claims to help people by restricting them. The often quoted satirical line comes to mind: “we’re from the government and we’re here to help.”

One of the prime targets of the bill is payday lending and the weapon is interest rate caps. Some instances would warrant a rate cap, but the idea makes little sense here.

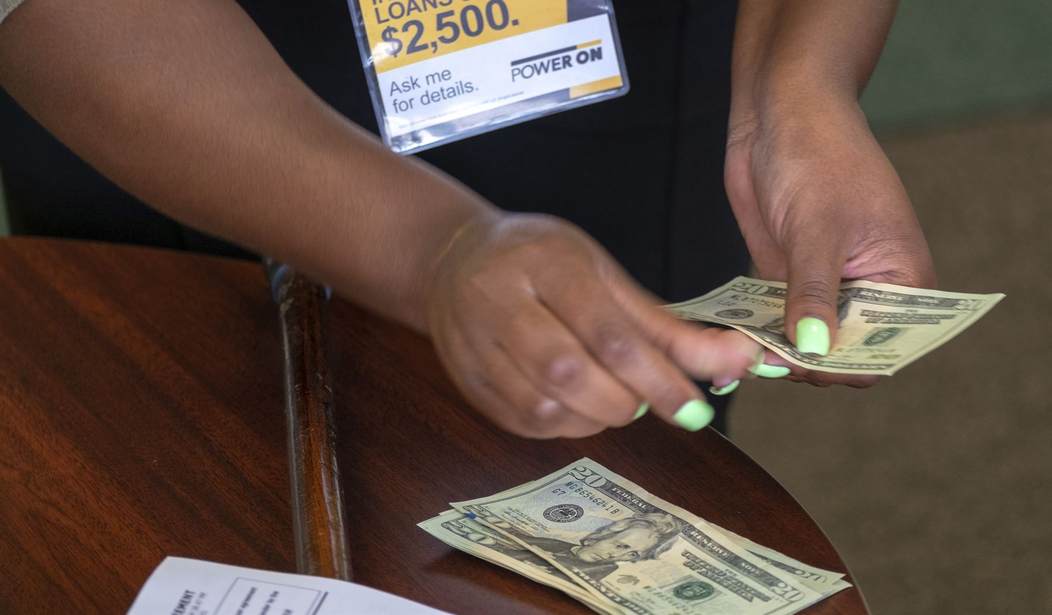

The bill proposes an annual percentage rate cap of 36 percent. In the mortgage market, for example, this percentage is above the market rate. However, for a two-week, $100 payday loan this translates to $1.38. This buck and change must cover the wages, rent, interest the lender has to pay to acquire the funds, and the losses from the loans that don’t get repaid. Clearly, the payday-loan fee needs to compensate for more liability than what $1.38 will cover.

Putting this into context our national legislators and their staff might understand, the total charge for this loan would be less than the expected tip for a single Capitol Hill cocktail. Yes, the norm for cocktails in our Nation’s Capital is $10-$20. Add to that a two to four-dollar tip. So, those sponsoring the payday-loan fee cap think there should be a national law prohibiting a payday lender from charging more for a two-week loan than what these same lawmakers voluntarily tip for one drink.

All of a sudden “mixologist” sounds a lot more profitable than “loan officer.”

Whether all the payday lenders would become bartenders with the cap in place isn’t clear, but in those states with similar caps, all of the payday lenders became something else. In every state with the 36 APR cap already in place, the payday-loan industry has collapsed.

Many would say “good riddance” when the payday-loan industry collapses. This distaste for payday lenders is especially strong among those who have never needed one. However, eliminating options does not help those who find themselves in a sudden financial bind.

A recent Federal Reserve Board study found that over 40 percent of U.S. adults do not have enough financial cushion to absorb a $400 emergency expense. Of those who do not have the savings to pay the $400, slightly over half would add to their carried-over credit card balance or take out a bank loan. But many do not have those options.

Another study found that in 2017 over 20 million people lived in households that had neither a savings nor checking account. For them, the options to meet emergency expenses are even more limited. The Federal Reserve Board study found that those who do not have the savings and cannot get a bank loan or run a higher credit-card balance will do things like skip payments on loans or utility bills or simply not pay the emergency expense. The financial penalties for these actions can be much higher than a payday-loan fee. Translated to an annual percentage rate, the penalty fees from bouncing a check can exceed 1,300 percent. Fees for reconnecting utilities can run to hundreds of dollars per incident.

What superior options does the Fair Credit Act offer in place of the payday-loan option it eliminates? None. The bill is eight pages of amendments to existing consumer-credit legislation that provides new penalties, but no help for those who, on occasion, depend on payday loans.

What actually happens when payday lending is driven out by government rate caps? Research published in the prestigious Journal of Law and Economics finds no evidence of payday borrowers switching to more affordable borrowing options. Instead, the research shows borrowers are forced into worse choices. For instance, pawn-shop borrowing was 60 percent higher in states that banned payday loans than in states with payday lending. Even worse was the impact on checking account closures. The researchers estimate that states with payday-loan bans saw a tripling of involuntary checking account closures—a crippling financial impact. This is likely from the use of bounced checks as a substitute for payday loans.

Forcing payday lenders to work for tips, as it were, will eliminate an industry and increase the financial distress among the most vulnerable borrowers. There’s nothing fair about that—especially for the borrowers the legislation is intended to help.

Join the Conversation

VIP members get the ability to comment on articles.